1. Digital Lenders in Kenya to Support Financial Inclusion and End Poverty

Financial services are a critical component of any economy. This is proven by the fact that both the global and national economies have set out programs to alleviate poverty, one of which is to build a financial sector and make services available to everybody. The financial sector's role is to allocate resources inside the market. However, only a small proportion of Kenya's population has access to official financial services. Poverty is more than a lack of income, and exclusion from formal financial services is one of its manifestations. Financial inclusion is one strategy to ensure that a country's economic growth is inclusive. The Kenyan government's Blueprint Vision 2030 effort aims to lower the proportion of the population without access to financing from 85% to less than 70%.5 Financial inclusion should allow previously excluded people, the poor, the unserved, and the underserved, to get access to financial products. Financial inclusion encompasses all efforts to make formal financial services available, accessible, and cheap to all segments of society. The efforts are intended to target a segment of the population that has previously been excluded for various reasons. People who fall into this category are known as the underserved or the unserved. Financial inclusion efforts necessitate that institutions tap on this population's potential by providing financial services to them. Private institutions may and should make efforts to increase financial inclusion. Private enterprises should be involved in the development of market-based solutions for the world's poorest consumers, those at the bottom of the pyramid. The bottom of the pyramid refers to individuals who are financially excluded and are unserved or underserved by the vast organized private sector. Serving them necessitates technological, product, and service innovation, as well as new business strategies. Kenya has seen technological innovation in the financial sector, particularly in the lending market via digital credit. Prior to the emergence of digital credit, most Kenyans relied on informal lenders (shylocks) as well as relatives and friends for credit. The banking industry exclusively served the wealthy or those with collateral who could afford to pay the fees and visit the bank branches. Banking organizations had little motivation to assist the poor because their products were not only pricey but also inaccessible to them. However, the arrival of digital credit has changed everything. Digital credit is a type of digital banking product that includes little in-person contact and relies on digital infrastructure. The solution uses digital infrastructure to receive loan applications, determine borrowers' creditworthiness, authorize the loan, disburse funds, and receive payment. Digital credit products are those that rely on digital infrastructure for the entire or even a portion of the procedure. The digital infrastructure used by these items, combined with their ease, has resulted in their enormous market demand.

2. Digital Credits Characteristics

Digital credit has four major properties. First, current digital access enables loan eligibility. A bank account or a credit history are not required to obtain a loan. Most products need borrowers to already have mobile phone or mobile money service subscriptions, as well as social media accounts. Second, lending choices are computerized and rely on non-traditional data. The digital providers take the position that all data is credit data. They utilize different algorithms to determine the creditworthiness of consumers who do not have a credit history. Data such as mobile phone usage, mobile payment usage, airtime usage, and information from social media profiles are used. This approach replaces manual decision-making. The third feature is that the loans are available immediately. This is because the decision to issue the loan is automated. If the borrower is approved for a loan, the funds are usually disbursed within five minutes of the request. This distinguishes it from regular bank loans, which might take a lengthy time to get granted. The fourth aspect is that, due to the target market, the loans are short term and high risk. The products are offered to the unbanked population, who lacks credit history and collateral, making the items more expensive. The fact that these loans are taken out during emergencies or while consumers wait for their next month's salary contributes to their short-term nature. In Kenya, digital credit is available through four business formats. The collaboration between banks or microfinance institutions and mobile network operators (MNO) is the most frequent and pioneering business model. MNOs provide credit algorithms based on data obtained from knowing your customer's needs. They use the information they have on their clients to create a method for determining creditworthiness. Second, MNOs serve as vehicles for loan disbursement, loan collection, and client interaction. Banks or financial organizations manage customer accounts, provide lending capital, and accept high-risk deposits. Safaricom M-Pesa and Commercial Bank of Africa (CBA) provide MShwari, Safaricom M-Pesa and Kenya Commercial Bank (KCB) give KCB-M-Pesa loans, while Airtel Money and Faulu Bank provide Kopa chapaa loans. Application-based digital credit is the second business model. This refers to businesses that make loans in their own names without partnering with a financial institution. Borrowers are required to install an app and provide their social media credentials. The app tracks mobile phone and mobile money usage, as well as social media activity. They can estimate the creditworthiness of the borrowers based on this information. Tala, Branch, and Saida loans are examples of such lenders in Kenya. The final business model, however uncommon, is a bank that provides digital services. This resulted from the CBK's licensing of Mobile Virtual Network Operators (MVNO). Banks do not require collaboration with mobile network operators as they build their own digital infrastructure. Equittel, for example, is a subsidiary of Equity Bank. Airtel Kenya leases their telecommunications infrastructure. The variety of digital credit as well as product innovation demonstrates efforts to provide credit to the unbanked population in order to deepen financial inclusion. Financial inclusion extends beyond enhanced credit availability to include a well-functioning infrastructure that allows individuals to access credit while also preserving their rights. However, credit to these vulnerable people must be managed in order to avoid unexpected outcomes such as over-indebtedness, which is a cause of poverty. Furthermore, digital credit can help users gain access to formal financial services. However, if lending is not monitored, there is a risk of predatory lending, in which consumers are unable to pay, resulting in poor credit ratings and limiting their access to formal financial services. Thus, if such lending is not regulated, firms will benefit at the expense of consumer rights, which runs counter to financial inclusion initiatives.

3. The Importance of Regulation

a. Charging High Interest

It is difficult for profit-seeking enterprises supplying goods and services to exhibit self-control when charging high-interest rates where there are vulnerable consumers. Digital credit lenders provide a product to a group of people who would not otherwise have access to such items. As a result, such persons can be exploited by charging exorbitant interest rates. The high interest rate is due to the considerable risk of lending to the underserved. M-Shwari, the biggest digital credit provider, levies a monthly facilitation fee of 7.5% on each loan. If the loan is not paid within one month, a facilitation fee is applied to the outstanding sum. If this is calculated annually, the loan is subject to a facilitation fee of 138% per year. Other digital credit companies, like traditional banking institutions, offer relatively high interest rates. Tala Loan, an app-based service provider, charges a monthly service fee ranging from 11-15%. This means that digital credit is exceedingly expensive, increasing the likelihood of default or the incapacity of borrowers to repay the loans. Simple access to a variety of loans Consumers tend to borrow from the many banks offering digital credit since the nature of the loan is quick. Borrowers use multiple borrowing to put together the lump quantity they believe they require. The lenders have no means of knowing that the borrowers have multiple loans from various institutions. Some regulated lenders are obligated to report to the credit bureau, while non-financial organizations are not, making it difficult for other lenders to know about customers' outstanding loans. Furthermore, while establishing creditworthiness, some of these institutions exclude information from the credit rating bureau.

b. Failure to disclose Prices, Terms and Conditions

Lack of openness on costs, terms and conditions on users, particularly poor and low-income individuals, as well as a lack of awareness of both digital networks and financial goods. Users are not always forced to read terms of service agreements and are not always financially literate. Before offering services, providers frequently fail to provide information. As a result, users make poor financial judgments since they do not completely understand the product and its underlying terms and conditions. The lender is unable to access certain terms and conditions. Many digital lenders only provide access to product terms and conditions via a web link, which cannot be accessed directly via the channel the consumer uses to borrow, which is on the mobile platform, unless the borrower has a smartphone and mobile data. However, many borrowers, particularly those in rural areas, do not own smartphones. This makes reading the terms and conditions difficult, if not impossible, for the borrower.

c. Strict Penalties for Borrowers

On the other side, there are severe consequences for failing to pay the digital credit, which is a service given for individuals who are unable to access formal services. Borrowers are initially eligible for loans depending on the lender's algorithms. However, consumers default due to a variety of issues such as high interest rates, multiple borrowing, inadvertent borrowing, or a lack of comprehension of the terms. The penalty for failure and late payments can be severe. For example, if a consumer repays a loan after the required period has passed, they will be prohibited future loans from that institution. According to several FinAccess household surveys, the adult population of Kenya borrowing from unregulated digital lenders climbed from 200,000 in 2016 to 2 million in 2019. However, the number of borrowers fell to 600,000 by 2021, presumably as a result of the negative effects of the COVID-19 pandemic, which was exacerbated by increased negative listing of borrowers by Credit Reference Bureaus (CRBs) due to income disruptions that impaired loan repayments.

4. 4. Privacy

Violation: Data Breach in 2019

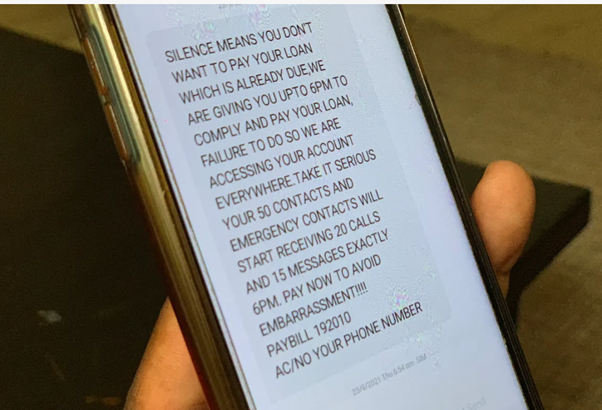

5. 5.Privacy

Violation: Terror on Borrowers who cannot Pay the Loans

Conclusion

Based on the description above, it is strongly urged that the Kenyan government enact the Data Regulation Law in order to preserve the privacy of customers. Lenders have violated borrowers' privacy by accessing their contact and social media information to guarantee they can repay the loan (credit worthiness). Furthermore, they use the contact to threaten and terrorize consumers who are unable to pay. Customers are also burdened by the exorbitant interest rates charged by digital lenders.